Summary - OTP Group’s First quarter 2026 results

published atMay 15, 2026Tags:results

Summary - OTP Group’s First quarter 2026 results

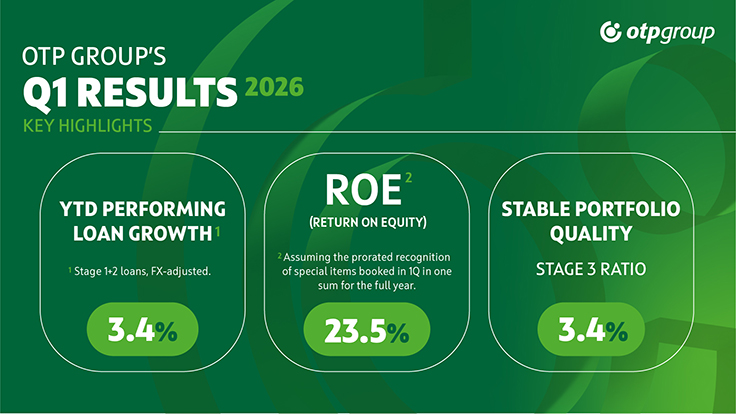

OTP Group started 2026 with strong underlying banking performance. Profit after tax amounted to HUF 324 billion/EUR 845 millionin 1Q 2026, up 9% y-o-y, with ROE reaching 23.5% with the prorated recognition of special items booked in a lump sum at the beginning of the year. The reported consolidated profit after tax amounted to HUF 177 billion/EUR 461 million, mainly reflecting the front-loaded impact of special taxes and supervisory fees.

Profit before tax increased by 12% y-o-y, while operating profit rose by 7% in HUF terms and by 10% on an FX-adjusted basis. Total income grew by 9% y-o-y, driven by the increase in net interest income reflecting both the continued dynamic expansion of business volumes and the improvement in net interest margin. The favourable margin development in 1Q was partly driven by the q-o-q improvements in several key markets, including the Eurozone subsidiaries and Uzbekistan.

Operating expenses increased by 13% y-o-y, or

by 17% on an FX-adjusted basis. The rise was mainly linked to wage inflation,

higher depreciation related to IT investments, and growing IT infrastructure, as

well as software and marketing costs. Even so, the cost-to-income ratio

remained moderate at 42.3%.

The risk profile remained favourable: the Stage 3 loan ratio declined by 0.1 pp q-o-q and improved to 3.5% by end-March. As a result, the quarterly credit risk cost ratio stood at 47 bps.

Lending momentum remained strong. Consolidated performing (Stage 1+2) customer loans grew by more than 3% in the first quarter and by 16% y-o-y (FX-adjusted). Mortgage lending continued to be a standout areain the first quarter, with a 6% q-o-q increase at group level and a 10% rise at OTP Core, supported by Hungary’s Home Start Programme. Consumer loans and corporate loans also continued to expand.

Customer deposits increased by 3% q-o-q and by 11% y-o-y on an FX-adjusted basis. The Group’s net loan-to-deposit ratio stayed unchanged at 77%, confirming a balanced and stable funding structure.

OTP Group maintained its strong capital position. At the end of March 2026, the CET1 ratio stood at 17.6%, while the total capital adequacy ratio was 19.2%. With the prorated recognition of annual special items, the CET1 ratio would have been 17.9%.

Management does not consider it necessary to revise its guidance for the Group’s 2026 performance. FX-adjusted organic growth in performing loans may remain around the approximately 15% level achieved in 2025, while the net interest margin may stay close to the 2025 level of 4.34%. The cost-to-income ratio may be somewhat higher than in 2025, while the credit risk profile is expected to remain broadly similar.